For nearly eight decades, the U.S. dollar has been the foundation of international trade. From commodities such as oil and copper to global investments and reserves, it remains the most widely used currency in the world.

However, as the global economy becomes more interconnected and technologically advanced, new questions are emerging about whether the dollar’s dominant role will, or should, continue. This article explores both sides of the debate in clear, practical terms.

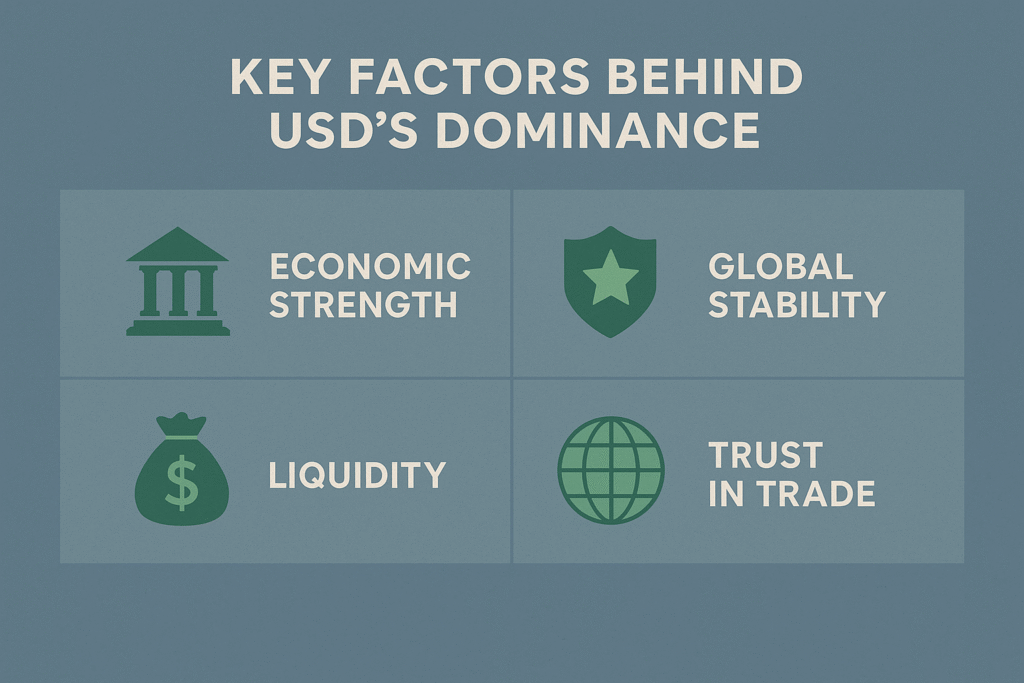

The U.S. dollar became the central trading currency after World War II, when nations sought a stable anchor for global commerce. America’s strong economy, transparent legal system, and well-regulated financial markets gave the dollar long-term credibility.

In everyday terms, this means that when a Japanese importer buys copper from Chile, both sides prefer to settle the payment in dollars. Using one common, trusted currency avoids multiple conversions and exchange-rate risks, making trade faster and more predictable.

The dollar provides a consistent benchmark for valuing goods and contracts. This reliability helps businesses, investors, and governments plan ahead without worrying about sudden currency swings.

Liquidity simply means how easily money flows through markets. U.S. bond and money markets are the largest and most active in the world, which makes it easy for investors and central banks to buy and sell dollar assets.

During times of financial turmoil, such as the 2008 Global Financial Crisis or the COVID-19 pandemic, the U.S. Federal Reserve extended swap lines (temporary lending arrangements) to foreign central banks. This ensured that dollars kept circulating and global trade did not freeze.

Because so many international payments move through U.S.-linked banks, the United States can impose sanctions and monitor transactions worldwide. Critics argue that this creates an uneven distribution of power in the global financial system.

Many emerging economies borrow in U.S. dollars. When the Federal Reserve raises interest rates, the cost of that borrowing rises, sometimes leading to debt distress in other countries.

Easy access to cheap credit can also encourage excessive borrowing at home. Over time, this dependence may undermine fiscal discipline and create vulnerabilities if demand for dollars declines.

The landscape is slowly shifting. The Chinese yuan is increasingly used in Asian trade; the euro remains a strong alternative within Europe; and digital currencies such as central-bank digital currencies (CBDCs) are being developed to make cross-border payments faster and cheaper.

Still, replacing the dollar entirely is difficult. Trust, legal consistency, and scale cannot be replicated overnight. A multi-currency world could bring diversity, but also more volatility and higher transaction costs.

A gradual evolution toward a multipolar currency system, where several major currencies share influence, could give countries more flexibility and autonomy.

Yet, such a system might also complicate crisis management. Without a single, globally accepted reserve currency, coordinated responses to market shocks would be harder to achieve.

The ongoing debate is less about replacing the dollar and more about creating a fair and resilient international monetary framework. Policymakers must weigh stability against national sovereignty, ensuring that no single economy bears or wields disproportionate power.

The U.S. dollar’s dominance has supported global stability and efficiency for decades, but it also raises legitimate concerns about dependence and inequality. As global trade evolves, the most likely outcome is not sudden change, but gradual adjustment.

A more balanced financial system, one that maintains confidence, transparency, and cooperation, could ultimately serve both the United States and the broader international community,

We use cookies to give you the best online experience. By agreeing you accept the use of cookies in accordance with our cookie policy.